Tuesday, July 12, 2011

Note to self

I submitted an insurance claim today for diabetic pump supplies not covered by the grant and my most recent massage appointment.

Thursday, July 7, 2011

It's been a while

I have a lot to say. At $40, the pedicure was disappointing. The polish smeared before I left the salon, and I still have visible callouses. I'll go back to doing it myself.

I suspect there's a $600 grant cheque from the Ontario government in my purse to offset insulin pump supply costs. It's been so busy lately; I've had no time for envelope opening.

My gas consumption is increasing rapidly, as are my thoughts and desire to take the car completely off the road, and live car free.

On the brighter side, July is my $400 daycare month. My increased evening care expenses should in principle bother me slightly less.

I sold off my Bluesfest pass at a serious discount for $100 and reduced my anticipated need for evening sitter services.

Not enough time to grocery shop either. I'm buying my lunch at work, and any shopping that does get done is limited to unplanned impulse selection of prepared foods from Farm Boy which increases the average cost of a meal at home.

I finally remembered to expense the business lunch. Work insurance covered most of my dental checkup. I need to make a short list of financial decisions required before my job winds down in August. My medical benefits carry into October.

Now I need to remember to expense today's massage appointment, and the portion of the diabetic supplies not covered by the $600 cheque. Which reminds me, I've got to track down the receipt for the diabetic supplies.

The mail strike inadvertently disrupted the flow of my diabetic pump supplies when the courier got overloaded and lost the package. I consumed fewer supplies during this period.

I am a creature of habit, and I am ever so hopeful that the habits I've worked so hard in acquiring over the course of maintaining this diary will serve me well during the transition.

It is strange working out a notice period. I am grateful, yet lack focus. At the same time, between new guy and networking, my social calendar overfloweth... Nice problems to have.

New blouse, new dress, new iPhone 4, new bike helmets and life jackets for the children.

More soon. My conversational French as well as my confidence are improving.

I suspect there's a $600 grant cheque from the Ontario government in my purse to offset insulin pump supply costs. It's been so busy lately; I've had no time for envelope opening.

My gas consumption is increasing rapidly, as are my thoughts and desire to take the car completely off the road, and live car free.

On the brighter side, July is my $400 daycare month. My increased evening care expenses should in principle bother me slightly less.

I sold off my Bluesfest pass at a serious discount for $100 and reduced my anticipated need for evening sitter services.

Not enough time to grocery shop either. I'm buying my lunch at work, and any shopping that does get done is limited to unplanned impulse selection of prepared foods from Farm Boy which increases the average cost of a meal at home.

I finally remembered to expense the business lunch. Work insurance covered most of my dental checkup. I need to make a short list of financial decisions required before my job winds down in August. My medical benefits carry into October.

Now I need to remember to expense today's massage appointment, and the portion of the diabetic supplies not covered by the $600 cheque. Which reminds me, I've got to track down the receipt for the diabetic supplies.

The mail strike inadvertently disrupted the flow of my diabetic pump supplies when the courier got overloaded and lost the package. I consumed fewer supplies during this period.

I am a creature of habit, and I am ever so hopeful that the habits I've worked so hard in acquiring over the course of maintaining this diary will serve me well during the transition.

It is strange working out a notice period. I am grateful, yet lack focus. At the same time, between new guy and networking, my social calendar overfloweth... Nice problems to have.

New blouse, new dress, new iPhone 4, new bike helmets and life jackets for the children.

More soon. My conversational French as well as my confidence are improving.

Wednesday, June 29, 2011

Oops.

Visa statement day: $3,278.78.

It looks a little crazier than it actually is, containing approximately $800 worth of expenses that I can get back. Note to self: Check the exact number and start the expense claims.

Just entered it into the spreadsheet, and it didn't break it. Whew.

It looks a little crazier than it actually is, containing approximately $800 worth of expenses that I can get back. Note to self: Check the exact number and start the expense claims.

Just entered it into the spreadsheet, and it didn't break it. Whew.

Monday, June 20, 2011

The power of money

The ATM dispensed two crisp $50 bills when I withdrew my petty cash on the weekend. I can't remember this ever happening before. Feels like a good omen.

Thursday, June 16, 2011

Don't worry, be happy

I attended a Sun Life retirement webinar sponsored by my current employer this week. According to their retirement planner tool, I need to save up just short of $1 000 000.

This is not a problem I can solve today.

This is not a problem I can solve today.

Tuesday, June 14, 2011

Good faith

I have stopped my RRSP payroll deductions. It could be one or two pay periods before the change will take effect. These are before tax dollars. The payroll department could not act directly on my instruction; I had to call Sun Life to sort it out.

The amount in my DPSP is $5163.25. It will not vest before I leave (not mine to keep).

The RRSP value is higher: $25538.64. I have absolutely no idea how I saved this amount, but I'll move it to the plus column. When I spoke to the Sun Life representative, she mentioned that their fees are generally lower than other plans and got me thinking about consolidating this amount with my Assante managed plan.

The amount in my DPSP is $5163.25. It will not vest before I leave (not mine to keep).

The RRSP value is higher: $25538.64. I have absolutely no idea how I saved this amount, but I'll move it to the plus column. When I spoke to the Sun Life representative, she mentioned that their fees are generally lower than other plans and got me thinking about consolidating this amount with my Assante managed plan.

Monday, June 13, 2011

Uggh.

I just spent $US 33.52 per year on establishing a new web presence under my own name, rather than my existing corporate name. It looks like I need to set up budget parameters to support my job search.

Saturday, June 11, 2011

Priorities

I spent $300 for 25 bottles of wine at the SAQ depot this afternoon. That's $12 per bottle. I don't want to run out for the foreseeable future (and it's a nice Friday gift for the caregiver). It's a bit of a drive, so I made it worth the trip.

On the way home, I stopped at Shoppers Drug Mart to take advantage of the $8 sale price on a L'Oreal hair colouring kit. It needs to be done in the next few weeks unless I want the grey to take over, and I'll certainly be doing it myself. Gray is gone now; hooray for me!

I paid $20 this morning to register both girls for Chinese school in September. The $150 registration fee for Girl Guides will appear on my next Visa statement. I'm thinking about adding music lessons for my youngest, but for now it's just a thought.

All iTunes and iPad apps are back on the No list. The jury's still out on sporting goods.

I decided to splurge on a $72 six-month membership to the meetup service to advertise networking events through my business. I'm on the fence about bringing the business back into the foreground, but I'd like a better idea of what the choices really are in 2011.

There is still much thinking and prioritizing to do. Je voudrais une pédicure... I should probably turn my work-related RRSP contributions off completely. The interest rate is lousy, and the employer match does not pay out until I've been on staff for two years.

Update, June 13:

I instructed payroll to turn off my RRSP contributions today.

On the way home, I stopped at Shoppers Drug Mart to take advantage of the $8 sale price on a L'Oreal hair colouring kit. It needs to be done in the next few weeks unless I want the grey to take over, and I'll certainly be doing it myself. Gray is gone now; hooray for me!

I paid $20 this morning to register both girls for Chinese school in September. The $150 registration fee for Girl Guides will appear on my next Visa statement. I'm thinking about adding music lessons for my youngest, but for now it's just a thought.

All iTunes and iPad apps are back on the No list. The jury's still out on sporting goods.

I decided to splurge on a $72 six-month membership to the meetup service to advertise networking events through my business. I'm on the fence about bringing the business back into the foreground, but I'd like a better idea of what the choices really are in 2011.

There is still much thinking and prioritizing to do. Je voudrais une pédicure... I should probably turn my work-related RRSP contributions off completely. The interest rate is lousy, and the employer match does not pay out until I've been on staff for two years.

Update, June 13:

I instructed payroll to turn off my RRSP contributions today.

Turn, turn, turn

On Thursday, I will learn that I am losing my job on August 19. With this news will come a package as well as eligibility to apply for employment insurance should the need arise.

With the credit line debt squared away, and the bulk of the daycare burden behind me, I am reflecting on the pros and cons of such a change. I have not shared the news with my kids.

I told them in the car on the way to Chinese school this morning. They were calm.

With the credit line debt squared away, and the bulk of the daycare burden behind me, I am reflecting on the pros and cons of such a change. I have not shared the news with my kids.

I told them in the car on the way to Chinese school this morning. They were calm.

Monday, June 6, 2011

More weekend highlights

The good:

- A free family pass to the Ottawa international children's festival (courtesy my next-door neighbour) with the unexpected treat to an exceptional performance of With a Doll in Her Pocket by Italy's Teatro delle Briciole

- Indulging in $7 worth of ice cream at the festival

- A simple Saturday morning brunch with a friend (his turn to treat)

- Geocaching, swimming, and bike riding with my youngest (and a picnic)

- Two pop-in visits with rarely visited friends just because their Facebook feeds were interesting

- Mowing the lawn and organizing the garage

- Noticing the pharmacy provided only one vial of insulin for the price of four, and calling to correct the error

- Caving into a whim that cost us $28 for mediocre dim sum, most unappetizing when served cold. Even the tea was undrinkable, with sediment floating in it.

- Forgetting to buy groceries

Submitting an insurance claim for last week's massage appointment- Switching as many of my accounts over to e-bills as possible

- Organizing receipts

Friday, June 3, 2011

Corruption and greed

On the subject of a homeland visit to the village in Anhui, China where my eldest was born, I've just decided that we won't be signing up any time soon, even though the 10-year savings bond I purchased to cover her airfare for said visit is maturing in September.

Today I learned the orphanage director personally requests a $US 1000 cash donation, and the orphanage tour now includes a personally-escorted visit to a nearby ATM machine.

So disappointed for the children, and saddened by this news.

Today I learned the orphanage director personally requests a $US 1000 cash donation, and the orphanage tour now includes a personally-escorted visit to a nearby ATM machine.

So disappointed for the children, and saddened by this news.

A second opinion

On the theme of dental work, I decided to switch my youngest over from the services of the pediatric dentist to my own dentist. (I called Standard Life first to confirm she was covered for checkups at six month intervals.)

He's been my dentist for twenty years. I tried switching when I moved to Kanata nearly five years ago, but I promptly switched back. He's good, he's patient, he's kind, and he doesn't overcharge either. I was lucky to get a next day appointment for her!

On the subject of the enamel deficiency (related to early-years malnutrition), his opinion was the same as the pediatric dentist. It's surface level damage only, restricted to the baby teeth. Her adult teeth should not be affected.

On the subject of replacing the spacer (initially placed by the pediatric dentist), he thinks we might need to introduce a retainer instead, but not for a few years. It had fallen out, and his advice was to leave it for now. Several of her baby teeth were missing when she joined this family. They may have been extracted, although it's something we'll never really know. It was too soon for them to fall out on their own.

On the subject of 6-year molars, his advice is to seal them once they are completely in.

Deciding not to seal the molars of my eldest turned out to be very costly in the long run, and she had to undergo various rounds of anaesthesia and multiple fillings. I hope to avoid it this time if that's possible.

On the subject of braces, she's likely to need them. We'll revisit this later, but it's good information to have in advance and helps with longer term financial planning. Standard Life has a lifetime orthodontics limit of $1500 on my current policy. It will help a little. I'll need to factor this information into any future decision to change jobs!

He asked if the pediatric dentist had done x-rays, and if she'd seen anything. I answered that she did them, and not noted any specific areas of concern. He did not redo them.

He's been my dentist for twenty years. I tried switching when I moved to Kanata nearly five years ago, but I promptly switched back. He's good, he's patient, he's kind, and he doesn't overcharge either. I was lucky to get a next day appointment for her!

On the subject of the enamel deficiency (related to early-years malnutrition), his opinion was the same as the pediatric dentist. It's surface level damage only, restricted to the baby teeth. Her adult teeth should not be affected.

On the subject of replacing the spacer (initially placed by the pediatric dentist), he thinks we might need to introduce a retainer instead, but not for a few years. It had fallen out, and his advice was to leave it for now. Several of her baby teeth were missing when she joined this family. They may have been extracted, although it's something we'll never really know. It was too soon for them to fall out on their own.

On the subject of 6-year molars, his advice is to seal them once they are completely in.

Deciding not to seal the molars of my eldest turned out to be very costly in the long run, and she had to undergo various rounds of anaesthesia and multiple fillings. I hope to avoid it this time if that's possible.

On the subject of braces, she's likely to need them. We'll revisit this later, but it's good information to have in advance and helps with longer term financial planning. Standard Life has a lifetime orthodontics limit of $1500 on my current policy. It will help a little. I'll need to factor this information into any future decision to change jobs!

He asked if the pediatric dentist had done x-rays, and if she'd seen anything. I answered that she did them, and not noted any specific areas of concern. He did not redo them.

Friday, May 27, 2011

I fall to pieces

My Ironman Triathlon watchband has been crumbling. I've had it for a while. I love its alarms and its interval timer. I recently went back to the store where I had purchased it from. They gave me two options: fix it myself (be creative) or buy a new one for $90. I thought at first that Crazy Glue might work, until I realized I don't have all of the pieces.

Today while I was picking up my race kit for tomorrow's 10K running event, I had to detour through the race expo to exit the building. It's how they set it up in case I might want or need more sporting goods. I was tempted. They have nice stuff and good promotions.

I noticed a Timex booth promoting the kind of watch that I'm wearing. I stopped to chat and learned that I can go back to the store and ask for the postage-paid envelope the vendor has provided specifically for this purpose. The problem is known to the vendor and they are willing to assess it at no charge and give me an additional point of view on my options.

Today while I was picking up my race kit for tomorrow's 10K running event, I had to detour through the race expo to exit the building. It's how they set it up in case I might want or need more sporting goods. I was tempted. They have nice stuff and good promotions.

I noticed a Timex booth promoting the kind of watch that I'm wearing. I stopped to chat and learned that I can go back to the store and ask for the postage-paid envelope the vendor has provided specifically for this purpose. The problem is known to the vendor and they are willing to assess it at no charge and give me an additional point of view on my options.

Car maintenance

Today it's raining hard; I'm working from home. It's Visa statement day. I've been holding back on a few non-pressing items to do with my car to defer the expense. I don't use it much during the week now. The change of seasons put my bike firmly back on the road.

It's a good day to have my snow tires switched back to the regular set. They are all on rims, which initially cost a lot, but I get it back in economies of time and I think it reduces overall labour costs. The mechanic is my friend's uncle. That's how I found him. Well, that and an unsolicited recommendation from a former co-worker who also uses his services.

He doesn't know that I know any of his relatives. He's just really nice. He decided not charge me to switch them over this year; it usually costs around $50 which includes tire storage. He did tell me that he pulled a nail from one of the tires and repaired it for me.

He advised me to keep an eye on the tire for pressure changes. He also pointed out that I've got one season left on the summer tires. Odds are good I'll buy the next set from him!

I don't drive much at night, so it hasn't bothered me that the passenger headlight burnt out a few months back. I had it replaced at the Kia dealership this morning at a cost of $65.74 on my way home. That seems like a lot to me. On the bright side, they were quick too.

I ran my gas tank down to empty last weekend, but did not need to refuel it with bike commuting all week. I stopped on the way back from the dealership: $60.11 for that!

It's a good day to have my snow tires switched back to the regular set. They are all on rims, which initially cost a lot, but I get it back in economies of time and I think it reduces overall labour costs. The mechanic is my friend's uncle. That's how I found him. Well, that and an unsolicited recommendation from a former co-worker who also uses his services.

He doesn't know that I know any of his relatives. He's just really nice. He decided not charge me to switch them over this year; it usually costs around $50 which includes tire storage. He did tell me that he pulled a nail from one of the tires and repaired it for me.

He advised me to keep an eye on the tire for pressure changes. He also pointed out that I've got one season left on the summer tires. Odds are good I'll buy the next set from him!

I don't drive much at night, so it hasn't bothered me that the passenger headlight burnt out a few months back. I had it replaced at the Kia dealership this morning at a cost of $65.74 on my way home. That seems like a lot to me. On the bright side, they were quick too.

I ran my gas tank down to empty last weekend, but did not need to refuel it with bike commuting all week. I stopped on the way back from the dealership: $60.11 for that!

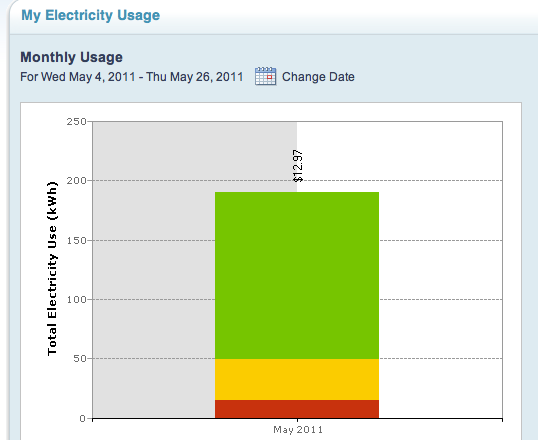

Thursday, May 26, 2011

Live in Ontario?

Hey, me too! I still receive my utility bills by mail, and tonight I am scrutinizing the hydro bill for sport. It contains a few inserts that merit further attention.

The first one is from the Ontario government, promoting the Ontario Clean Energy Benefit and promising 10% off my electricity bill for five years. I'm immediately suspicious.

To help you with the increased costs of these essential investments, the Ontario government has taken 10% off your electricity bill - including electricity costs, regulatory charges, the debt retirement charge and taxes.

Getting notice is good, I like that. After reviewing the additional material and scanning the details of my most current bill for items like the Debt Retirement Charge, I conclude the net result: my hydro costs are increasing noticeably after five years. I can wait.

The second insert introduces time-of-use (TOU) pricing. I need a better understanding of my habits and current rates before I can figure out what's involved here. I notice that it offers a calculator to help with the math. I clicked through but lost the trail.

There's a second letter, postmarked May 24, with An Important Notice About Your Electricity Rates on the envelope. It says the TOU rates will be introduced in four months time and offers a tool for viewing and comparing my electricity consumption patterns:

The first one is from the Ontario government, promoting the Ontario Clean Energy Benefit and promising 10% off my electricity bill for five years. I'm immediately suspicious.

To help you with the increased costs of these essential investments, the Ontario government has taken 10% off your electricity bill - including electricity costs, regulatory charges, the debt retirement charge and taxes.

Getting notice is good, I like that. After reviewing the additional material and scanning the details of my most current bill for items like the Debt Retirement Charge, I conclude the net result: my hydro costs are increasing noticeably after five years. I can wait.

The second insert introduces time-of-use (TOU) pricing. I need a better understanding of my habits and current rates before I can figure out what's involved here. I notice that it offers a calculator to help with the math. I clicked through but lost the trail.

There's a second letter, postmarked May 24, with An Important Notice About Your Electricity Rates on the envelope. It says the TOU rates will be introduced in four months time and offers a tool for viewing and comparing my electricity consumption patterns:

Monday, May 23, 2011

Long weekend highlights

Work was kind of stressful last week with colleagues visiting from California. We were in intense meetings all week long with working dinners on Tuesday and Wednesday. We also went for a team building event before dinner on Wednesday. I had some wine at dinner.

It was good work in a sense, yet four days without any real movement makes me kind of cranky. The meeting schedule was too compressed to permit me the luxury of my bike commute, noon run or midday swim. I intentionally left my weekend very open to recover.

With Chinese school cancelled for the long weekend, I spent three days completely in the company of my youngest child. At six, she is easily entertained (unlike her older sister).

We had Saturday morning coffee in the Maplelawn Public Garden. It's been a good year for rain, and the garden is a sheer delight. The day kind of meandered into a picnic over at Rockliffe Park with some geocaching, and we were able to fit in a short swim at the Brookstreet Hotel after a late dinner. The day's events cost us coffee and gas: under $15.

On Sunday, we went car free. The rain threatened all day, but held off until we completed our day trip by bicycle (and Chariot) to the Arboretum near Dow's Lake. We had initially set out for the Ornamental Gardens but never got there. Intoxicated by trees in bloom, we hit sensory overload and turned back, at most 1 km short of the gardens. While stopped for a picnic at Hartwell's Lock (along the Rideau Canal), we found the geocache. On the way home, we paused at Brittania Beach briefly to indulge in a snack for approximately $3.

Our route from Kanata took us through Watts Creek, along the Ottawa River parkway, then Pinecrest Creek, and eventually to the Experimental Farm pathway. I considered an alternate route home, but our Chariot is too wide to cross at Hartwell without disassembly.

Today was lower key, but cost a little more. At first light, I walked (while she biked) over to the library to return an unfinished book. We indulged in a longer swim, followed by a leisurely lunch of potato pancakes and tzatziki. Our afternoon revolved around some yard work, followed by a visit to the Parkdale Market for a hanging plant and some herbs for the garden: $32. I briefly considered a restaurant meal on a patio, but plants will give back.

I'm back to work in the morning.

It was good work in a sense, yet four days without any real movement makes me kind of cranky. The meeting schedule was too compressed to permit me the luxury of my bike commute, noon run or midday swim. I intentionally left my weekend very open to recover.

With Chinese school cancelled for the long weekend, I spent three days completely in the company of my youngest child. At six, she is easily entertained (unlike her older sister).

We had Saturday morning coffee in the Maplelawn Public Garden. It's been a good year for rain, and the garden is a sheer delight. The day kind of meandered into a picnic over at Rockliffe Park with some geocaching, and we were able to fit in a short swim at the Brookstreet Hotel after a late dinner. The day's events cost us coffee and gas: under $15.

On Sunday, we went car free. The rain threatened all day, but held off until we completed our day trip by bicycle (and Chariot) to the Arboretum near Dow's Lake. We had initially set out for the Ornamental Gardens but never got there. Intoxicated by trees in bloom, we hit sensory overload and turned back, at most 1 km short of the gardens. While stopped for a picnic at Hartwell's Lock (along the Rideau Canal), we found the geocache. On the way home, we paused at Brittania Beach briefly to indulge in a snack for approximately $3.

Our route from Kanata took us through Watts Creek, along the Ottawa River parkway, then Pinecrest Creek, and eventually to the Experimental Farm pathway. I considered an alternate route home, but our Chariot is too wide to cross at Hartwell without disassembly.

Today was lower key, but cost a little more. At first light, I walked (while she biked) over to the library to return an unfinished book. We indulged in a longer swim, followed by a leisurely lunch of potato pancakes and tzatziki. Our afternoon revolved around some yard work, followed by a visit to the Parkdale Market for a hanging plant and some herbs for the garden: $32. I briefly considered a restaurant meal on a patio, but plants will give back.

I'm back to work in the morning.

Saturday, May 21, 2011

Clothing and shoes

Truth be told I bought myself two new blouses from Winners last weekend, and some flip flops for the family at an Old Navy sale. Credit line is zeroed. Yes, I can.

I also paid $75 to the sitter for that visit to Le Nordik Spa on Sunday. Paradis sur terre.

I held back on coffee and wine all week, to take a small bite out of evening daycare costs. (We ran out of both last weekend.) I stocked up on wine last night, and on coffee today.

I also paid $75 to the sitter for that visit to Le Nordik Spa on Sunday. Paradis sur terre.

I held back on coffee and wine all week, to take a small bite out of evening daycare costs. (We ran out of both last weekend.) I stocked up on wine last night, and on coffee today.

Fun facts from the spreadsheet

I took a closer look at the spreadsheet data for the last twelve months:

- My requirement for petty cash averages $200 per month. I use it for evening sitters, music lessons, gum, concert tickets, and that sort of thing. Moving forward, I'll add a line item for it, to the month-ahead section of my spreadsheet.

- I spent $912 on interest alone servicing the Line of Credit. That's a lot.

- I spent $931 on hydro. That's approx $78 per month.

- Gas heat came in higher at $1262, which is more than I thought it was.

- Water came in lower at $515.

- I charged $32056 to my Aeroplan Visa gold card. That's enough points for a nice return trip somewhere, and it justifies the annual fee associated with the card.

Friday, May 13, 2011

Thursday, May 12, 2011

I've got a feeling

May the 15th falls on a Sunday this year. I care because it means tomorrow is payday. Last month, I reached the maximum annual deductions for CPP and EI premiums. I expect tomorrow's net pay to be adjusted accordingly. I suspect the amount of adjusting to contain the $100 I need to completely clear my credit line debt. It's not the end of the blog though.

The adoption loan balance of approximately $7000 waits patiently on deck. I might:

The adoption loan balance of approximately $7000 waits patiently on deck. I might:

- call the National Bank to determine the precise amount of the outstanding balance and if there is any fee associated with early paydown

- apply the proceeds from my sale of to-be-purchased ESPP shares in September

- increase the amount of my monthly payment starting October 1

Tuesday, May 10, 2011

What a difference a year makes

I am on track to kill this thing good and dead this Friday. Patience is key.

Saturday, May 7, 2011

Another day, another chart

This one nicely explains why the daycare expense has been my go-to thing to worry about this week. It drops considerably after Labour Day when my youngest starts full day school. The chart does not include costs for occasional evening or weekend babysitting.

|

| Daycare 2011 |

Wednesday, May 4, 2011

The book fair

The school is hosting a book fair this week. Both girls came home with $30 wish lists.

I was stunned, as I'd given them budget guidance of $10 each based on their ChoreBank balance and their Easter windfall from my parents. We live across the street from a public library and there are so many owned books in our home already they literally stick to my socks when I'm trying to navigate their collective clutter.

My eldest threw a tantrum when I explained $60 needs to be a budgeted item (and our budget priorities). I further explained how she could earn some of the money, and she sulked off to her room and closed the door. My youngest got the message right away and earned an additional $7 in an evening's worth of house chores.

The place looks great.

I was stunned, as I'd given them budget guidance of $10 each based on their ChoreBank balance and their Easter windfall from my parents. We live across the street from a public library and there are so many owned books in our home already they literally stick to my socks when I'm trying to navigate their collective clutter.

My eldest threw a tantrum when I explained $60 needs to be a budgeted item (and our budget priorities). I further explained how she could earn some of the money, and she sulked off to her room and closed the door. My youngest got the message right away and earned an additional $7 in an evening's worth of house chores.

The place looks great.

Monday, May 2, 2011

To infinity and beyond

Effective the pay period ending April 30, I have reached my statutory annual limits for both EI and CPP resulting in a net take-home pay gain of approximately $300 per month.

Update, May 3:

Daycare costs are higher in summer months with both girls out of school. The EI/CPP gain will offset some of these increased costs. The daycare landscape changes for the better in September when the youngest starts full-day school.

Update, May 6:

I did the math on summer daycare last night. Not pretty. I had been hatching a plan for a week away in late August. For $82.50, I've booked a camping weekend at Lac Phillippe.

Update, May 3:

Daycare costs are higher in summer months with both girls out of school. The EI/CPP gain will offset some of these increased costs. The daycare landscape changes for the better in September when the youngest starts full-day school.

Update, May 6:

I did the math on summer daycare last night. Not pretty. I had been hatching a plan for a week away in late August. For $82.50, I've booked a camping weekend at Lac Phillippe.

Please read the letter

The question surrounding UCCB eligibility was bothering me.

I couldn't find precisely what I was looking for online (an answer to the question of month vs day vs year). For clarification, I went back to the letter my accountant had attached to my personal tax return, in which he states my entitlement to:

I couldn't find precisely what I was looking for online (an answer to the question of month vs day vs year). For clarification, I went back to the letter my accountant had attached to my personal tax return, in which he states my entitlement to:

- an Ontario sales tax transition benefit for 2011 of $335 (expected in June 2011)

- a child tax benefit of $1532 for the period from July 2011 to June 2012. (I will need to update the spreadsheet to indicate a decrease of $25 per month.)

- the UCCB of $400 for 2011

Sunday, May 1, 2011

Still no

I'll revisit this list once the credit line is zeroed:

The car needs servicing too. It's very drivable, as is. Perhaps it can wait until June, except maybe the snow tire removal.

- services related to hair and foot care (with permission to splurge on related products, provided they cost less than what might have been spent on services)

- out-of-town car travel will be limited to one cottage visit on the Big Rideau

- clothing and shoes

- sporting goods

- train travel

- electronics

- parking

The car needs servicing too. It's very drivable, as is. Perhaps it can wait until June, except maybe the snow tire removal.

Guilty pleasures

This post is on the subject of nail polish pens. I think they are a relatively new product. I bought three today. I noticed them at the drug store earlier this week at the regular price of nearly $10, which seemed a little high. They were on sale for $6.74 when I went back.

We spent our afternoon doing manicures and pedicures at home. Each pedicure I do at home saves me $40. My eldest has an artistic side; both her designs and ideas are fun. She used the pens to put tulips on top of my red polished toes, little hearts on her sister's fingers, and something more geometric on herself.

We spent our afternoon doing manicures and pedicures at home. Each pedicure I do at home saves me $40. My eldest has an artistic side; both her designs and ideas are fun. She used the pens to put tulips on top of my red polished toes, little hearts on her sister's fingers, and something more geometric on herself.

And now for something completely different

We've taken up geocaching. It's a big game of outdoor hide and seek with many invisible players. I'm not sure how it works in the winter, but it's something my family can do together on foot or by bike until then. I paid $US 30 for an annual membership and $9.99 for an iPhone app. We found two caches yesterday.

Friday, April 29, 2011

The gift horse

My water bill arrived today claiming boldly that I have consumed -28 cubic metres of water in the past two months. I am curious as to how this is possible, and I will attempt to get more information. The amount due is showing as -$72.66. I wonder if they hold onto it for next time, or if they put it back into the account from which it was directly withdrawn.

I like the last line on the statement a lot: Credit Balance - Do not pay.

You will receive a bill every two months. Every effort is made to read your meter three times a year but you may not always receive three based on actual reads in a year. Bills based on estimates are calculated on previous seasonal water usage and do not take into account a change of ownership/occupancy or weather fluctuations from year to year. The City reserves the right to correct billing errors at any time.

Update, May 2:

I called and asked. They can't put it back. They will hold it against a future bill.

I like the last line on the statement a lot: Credit Balance - Do not pay.

You will receive a bill every two months. Every effort is made to read your meter three times a year but you may not always receive three based on actual reads in a year. Bills based on estimates are calculated on previous seasonal water usage and do not take into account a change of ownership/occupancy or weather fluctuations from year to year. The City reserves the right to correct billing errors at any time.

Update, May 2:

I called and asked. They can't put it back. They will hold it against a future bill.

Thursday, April 28, 2011

Statement balance

April 27: $2566.38.

In which the annual fee of $120 makes its appearance in the last hour.

On the bright side, the $100 universal child care benefit cheque arrived yesterday.

Update, May 1:

I have an open question here about eligibility for these UCCB cheques. My youngest turned six a few weeks ago, and I thought it would disqualify us.

In which the annual fee of $120 makes its appearance in the last hour.

On the bright side, the $100 universal child care benefit cheque arrived yesterday.

Update, May 1:

I have an open question here about eligibility for these UCCB cheques. My youngest turned six a few weeks ago, and I thought it would disqualify us.

Wednesday, April 27, 2011

Paying the blues

It is not yet Visa statement day, which is a bit of a shame as the balance sits relatively high at $2406 and discounted Bluesfest passes go on pre-sale at noon today. Last month's statement day was March 27. I intend to buy a single pass this year: $247.

Tuesday, April 26, 2011

That's an order

I logged into etrade this morning to accept my recent RSU grant. Much to my surprise, I found myself placing a same-day sell order on some vested options that have been sitting around for a little while. It won't yield a lot of money, with estimated net proceeds of $444.47. However, it will reduce debt. I am good with that.

Update, April 29:

Actual proceeds will be $US 495.88.

Update, May 6:

The cheque was issued for $455.61.

Update, April 29:

Actual proceeds will be $US 495.88.

Update, May 6:

The cheque was issued for $455.61.

Friday, April 22, 2011

Fuel economy

In the city:

378 km

40.965 litres

$53.17

$1.298 / litre

Approximately 14 cents / km

9.227 km / litre

Approx 22 mpg

On the highway:

507 km

33.54 litres

$43.57

$1.299 / litre

Approx 9 cents / km

15.12 km / litre

Approx 36 mpg

The car is rated 22 mpg for city and 30 mpg for highway.

378 km

40.965 litres

$53.17

$1.298 / litre

Approximately 14 cents / km

9.227 km / litre

Approx 22 mpg

On the highway:

507 km

33.54 litres

$43.57

$1.299 / litre

Approx 9 cents / km

15.12 km / litre

Approx 36 mpg

The car is rated 22 mpg for city and 30 mpg for highway.

Wednesday, April 20, 2011

Tuesday, April 19, 2011

Some enchanted evening

Full moon. True story.

My youngest fell climbing up the stairs before dinner last night, and based on the plaintive wail, I suspected a broken bone. We went straight to the nearest clinic, but it was closed. From there we practically flew over to the nearest open clinic, where her Ontario health card was promptly refused. I was surprised to learn that it expired a few weeks ago.

There are many lingering complications related to my daughter's class of Canadian citizenship. When asked, I paid the $40 for the appointment. We spent our dinner hour in the clinic's waiting area, and that cost us our pocket change for peanut butter cups from the nearest vending machine (to bring my blood sugar levels up enough for the drive home.)

The injury turned out to be nothing more than a nasty bruise and thankfully did not require an x-ray. We were released by 6:45 pm and we stopped at Pesto's on the way home (an additional unbudgeted $25.) I treated her with a little Advil before bed. (supplies on hand)

This isn't a rant about unplanned costs or waiting times. It's a not so subtle reminder of how fortunate we are in Canada to not have to routinely budget for these items.

While Service Ontario was at a loss to explain what had happened with the health card, they were quick to resolve it this morning. I can get the cost of the appointment back.

Update, April 21:

I went back to the clinic with the new health card number to request the refund. They took the information that they needed to share with OHIP, and advised me to return to the clinic in 4 to 6 weeks (May 19 to June 2) to find out if OHIP had processed the refund. The clinic will repay me only after OHIP pays them.

My youngest fell climbing up the stairs before dinner last night, and based on the plaintive wail, I suspected a broken bone. We went straight to the nearest clinic, but it was closed. From there we practically flew over to the nearest open clinic, where her Ontario health card was promptly refused. I was surprised to learn that it expired a few weeks ago.

There are many lingering complications related to my daughter's class of Canadian citizenship. When asked, I paid the $40 for the appointment. We spent our dinner hour in the clinic's waiting area, and that cost us our pocket change for peanut butter cups from the nearest vending machine (to bring my blood sugar levels up enough for the drive home.)

The injury turned out to be nothing more than a nasty bruise and thankfully did not require an x-ray. We were released by 6:45 pm and we stopped at Pesto's on the way home (an additional unbudgeted $25.) I treated her with a little Advil before bed. (supplies on hand)

This isn't a rant about unplanned costs or waiting times. It's a not so subtle reminder of how fortunate we are in Canada to not have to routinely budget for these items.

While Service Ontario was at a loss to explain what had happened with the health card, they were quick to resolve it this morning. I can get the cost of the appointment back.

Update, April 21:

I went back to the clinic with the new health card number to request the refund. They took the information that they needed to share with OHIP, and advised me to return to the clinic in 4 to 6 weeks (May 19 to June 2) to find out if OHIP had processed the refund. The clinic will repay me only after OHIP pays them.

A quick whine about wine

I took up the habit after reading about it in a diabetic magazine in 2008, and I believe that it can contribute to a healthy lifestyle. No doubt there is a relationship between alcohol and blood sugar. For various reasons not strictly limited to time and money (and insulin pump calibration), I recently managed to last ten consecutive days without wine.

Saturday night arrived and I decided to try a glass. (The nurse did not set out any restrictions when we discussed the possibility at my last appointment.) I purchased one bottle ($14.95) from the nearest LCBO, and had two glasses after dinner.

My blood sugar dropped outrageously low on Sunday morning into the category of severe hypoglycemia. I can function under these circumstances but just barely. I wasn't sure it was the wine at first, so I tried a bit more on Sunday night, yielding more dramatic results.

I'm not stocking up for a while.

Update, April 20:

I got advice from the diabetic nurse on how to handle this situation. She suggests that I turn the pump down by 25% (for the rest of the night) right before I go to bed.

Update, April 21:

It worked.

Saturday night arrived and I decided to try a glass. (The nurse did not set out any restrictions when we discussed the possibility at my last appointment.) I purchased one bottle ($14.95) from the nearest LCBO, and had two glasses after dinner.

My blood sugar dropped outrageously low on Sunday morning into the category of severe hypoglycemia. I can function under these circumstances but just barely. I wasn't sure it was the wine at first, so I tried a bit more on Sunday night, yielding more dramatic results.

I'm not stocking up for a while.

Update, April 20:

I got advice from the diabetic nurse on how to handle this situation. She suggests that I turn the pump down by 25% (for the rest of the night) right before I go to bed.

Update, April 21:

It worked.

Sunday, April 17, 2011

The birthday party

Today was our Mad Hatter Tea Party with nine well-mannered children in attendance. Much to my surprise, I kept this event under the $50 budget:

I spent the $5 remainder on grocery store tulips. They are pink.

- Invitations made by hand from recycled materials: $0

- Pretzels, ice cream cones, ice cream, grapes, and two-bite cupcakes: $10

- Ziplocked garden seeds, kool-aid mix, and seaweed crackers for loot bags: $20

- Previously enjoyed Salvation Army tea cups and saucers: $15

- Clock craft from recycled materials: $0

- Borrowed costumes: $0

I spent the $5 remainder on grocery store tulips. They are pink.

Friday, April 15, 2011

The savings account

I received a statement from ING Direct today, reminding me that I have been accumulating money in a tax-free savings account. I just called them. There is no penalty or fee associated with transferring funds from this account to my primary account at the Royal Bank. It takes one to two business days to complete the transaction. I'm moving $500.

Payday

The changes I made to my RRSP deduction took effect today. As expected, my take home pay is now higher. When I changed up the appropriate cell on my tracking spreadsheet this morning, I learned that I had freed up $250 to apply to my Line of Credit.

I have just reduced the amount owing to $1750, after reminding myself that I had intentionally reduced the RSP deduction for this purpose. I must confess that I was very strongly tempted to indulge in non-budgeted items when I saw the new amount.

Recap on my reasoning:

The RSPs are currently earning 0% interest. Maintaining a credit line debt costs me approximately 6% in interest. I did not eliminate the RSP contribution entirely; rather, I just reduced it to the amount that my employer was prepared to match.

In reviewing my credit line statements this evening, I noticed that my credit line debt also costs me life insurance premiums. If there's no balance, then I don't pay them, but there is.

I have just reduced the amount owing to $1750, after reminding myself that I had intentionally reduced the RSP deduction for this purpose. I must confess that I was very strongly tempted to indulge in non-budgeted items when I saw the new amount.

Recap on my reasoning:

The RSPs are currently earning 0% interest. Maintaining a credit line debt costs me approximately 6% in interest. I did not eliminate the RSP contribution entirely; rather, I just reduced it to the amount that my employer was prepared to match.

In reviewing my credit line statements this evening, I noticed that my credit line debt also costs me life insurance premiums. If there's no balance, then I don't pay them, but there is.

Thursday, April 14, 2011

Next steps

- Organize receipts and statements from last few weeks.

Submit massage receipt to work insurance for $85 refund.Expense last week's farewell-to-coworker lunch for $100 refund.Chase down unpaid invoice for 2 hours of consulting work, done earlier this year.Remind self that the $883 spent to date on insulin pump supplies is reimbursable and will eventually be covered by work insurance and government grants.Roof repair, sooner than later (some shingles are loose, but not off).- Car maintenance (but not yet, because I might still need the snow tires).

Update, April 17:

My neigbour dropped by this evening. Some shingles are now off.

Update, April 19:

My first $600 grant cheque has arrived! I'll be submitting the remaining $283 to my work insurance plan in the morning.

Update, April 27:

I took advice from my neighbour and bought shingles from Home Depot. The vent blew off my roof.

Update, April 29:

We had a big windstorm last night, which compounded the problem: many shingles blew off. Holding off the repair turned out to be okay. My neighbour bought more shingles last night, and we hired a roofer to do the repair. We shared the expense of the roofer across four attached shared-roof neighbours, and we all had the work done at the same time (keeping the cost down). When I bought this home in 2006, my real estate agent suggested I eventually replace/upgrade the vent. It went missing in the storm. Now is the time. $337.

Row by row

I just transferred $5000 from my chequing account to my credit line, reducing the balance currently owed to $2000. I have also updated my tracking spreadsheet.

Tax refund: $5550.

Tax refund: $5550.

Wednesday, April 13, 2011

Miles and miles

In anticipation of scary Visa bill, I continue to look for other ways to cut back and reduce costs. I am consciously trying to limit my use of the car to situations where I am pressed for time or traveling with children. I've stopped idling too (which was pretty limited to waiting for kids to do up their seat belts). While it probably won't save much, it might save a little.

I've biked to and from the office twice this week and walked my daughter over to her daycare on those days. This week has been a good one for planning and combining trips. There wasn't much in my trunk, but I emptied it. It might help. I also set the Trip Meter to 0 km when I last filled my gas tank (45 L for $57), for a better understanding of fuel economy.

I carpooled with a coworker to a lunch event today and let him drive for a change. Lunch itself was kind of nice too - the friend we were meeting at Pesto's decided to treat!

Update, April 14:

I missed a turn (daydreaming) on this morning's drive in. I thought I could recover with an alternate route, but then I got lost and had to turn around. Sigh.

I've biked to and from the office twice this week and walked my daughter over to her daycare on those days. This week has been a good one for planning and combining trips. There wasn't much in my trunk, but I emptied it. It might help. I also set the Trip Meter to 0 km when I last filled my gas tank (45 L for $57), for a better understanding of fuel economy.

I carpooled with a coworker to a lunch event today and let him drive for a change. Lunch itself was kind of nice too - the friend we were meeting at Pesto's decided to treat!

Update, April 14:

I missed a turn (daydreaming) on this morning's drive in. I thought I could recover with an alternate route, but then I got lost and had to turn around. Sigh.

Sunday, April 10, 2011

Back in the saddle

Yesterday was a really nice day here. I hauled the bikes and accessories out from the garage into the driveway and started the spring tune-ups myself. (Last year's outsourced tune-ups contributed to May's Visa statement spike.) I needed an Allen key set for the project ($5 at Canadian Tire). I went to the bike shop first, but they wanted $20 for it!

My five-year old is nearly six now. I have an old Trail-a-bike in the garage that I acquired for my eldest years ago, but I'm not sure we ever used it. I got it second hand. I wonder what I was thinking when I decided to move it from my old house to this one. My eldest would have been to big by then to use it. My youngest would not yet have been on my radar.

I was successful in locating all of the components of the Trail-a-bike and determining how they should fit together. I removed the fender from my older bike to free up space for it, but then I got stuck at the bolt for the seat post. While it seems I might need another tool to release it, I also think it's been bolted too tight.

The post needs to come off temporarily so that I can slide the hitch for the trailer onto it. At first I thought the hitch worked more like a clamp, but it has no give to it. I'm going to have to ask for help to remove the seat post, or pay someone at the bike shop to do it for me.

I ran out of wine on Thursday. I am going to let that slide for a few days and see what happens. The coffee supply dropped dangerously low as well, but I've restocked it. I have managed to cut my coffee consumption in half since starting this blog in November.

Asking for help always seems to come at a higher price.

My five-year old is nearly six now. I have an old Trail-a-bike in the garage that I acquired for my eldest years ago, but I'm not sure we ever used it. I got it second hand. I wonder what I was thinking when I decided to move it from my old house to this one. My eldest would have been to big by then to use it. My youngest would not yet have been on my radar.

I was successful in locating all of the components of the Trail-a-bike and determining how they should fit together. I removed the fender from my older bike to free up space for it, but then I got stuck at the bolt for the seat post. While it seems I might need another tool to release it, I also think it's been bolted too tight.

The post needs to come off temporarily so that I can slide the hitch for the trailer onto it. At first I thought the hitch worked more like a clamp, but it has no give to it. I'm going to have to ask for help to remove the seat post, or pay someone at the bike shop to do it for me.

I ran out of wine on Thursday. I am going to let that slide for a few days and see what happens. The coffee supply dropped dangerously low as well, but I've restocked it. I have managed to cut my coffee consumption in half since starting this blog in November.

Asking for help always seems to come at a higher price.

Friday, April 8, 2011

Change of venue

I left the $40 NAC Gospel and Blues concert at intermission tonight, after paying $9.25 for parking. Not my scene and not my crowd. The pianist was fair enough, but the crowd was mostly comprised of the aging Baptist congregation from his church. I found it depressing.

From there, I headed over to the Raw Sugar Café (with free street parking), to check out their $10 act. I poked my head in the door, and it wasn't my scene either. It did not help that the bouncer hesitated when I asked if I could come in. I didn't. Sigh.

So I texted a male friend and availed myself of his white wine and a spot on his sofa. He's good company. No more, no less. Safe to say NAC is out of budget for a while.

I paid $30 for the sitter.

From there, I headed over to the Raw Sugar Café (with free street parking), to check out their $10 act. I poked my head in the door, and it wasn't my scene either. It did not help that the bouncer hesitated when I asked if I could come in. I didn't. Sigh.

So I texted a male friend and availed myself of his white wine and a spot on his sofa. He's good company. No more, no less. Safe to say NAC is out of budget for a while.

I paid $30 for the sitter.

Another day, another bonus

Yesterday I received word that I will be granted an additional 450 units of restricted stock options in mid-April. At today's price, that could be a net gain of almost $5000 even after half of the gross value goes to a tax deduction (if/when I exercise and sell them).

No word yet on the vesting schedule.

Update, April 12:

The vesting schedule for this grant is 25% per year over 4 years from the date of grant.

No word yet on the vesting schedule.

Update, April 12:

The vesting schedule for this grant is 25% per year over 4 years from the date of grant.

Wednesday, April 6, 2011

Down with the ship

I tried to call in sick on Monday. My mind is still very active, but my body wasn't working quite right. I was due back at the hospital for an insulin pump adjustment, and I had to leave a sick child at home alone to attend it. One thing I have noticed recently is that stress and fatigue serve to sharpen my judgement, rather than cloud or obscure it.

The Blackberry kept buzzing. So I overrode my better judgement and went into the office on Tuesday, and sent the child back to school. I was on my way back home by 1 pm. I booked myself a massage appointment. Work insurance pays for it. That, and paid sick days, are just two of many compelling reasons to stay employed there.

The Blackberry had other ideas, and by 1 pm, I had the laptop back on, and I could not get to my appointment. Work is really challenging these days. While the company itself appears healthy, the work problems I am facing are hard to solve on a good day. We are understaffed, and creative solutions can only stretch my team so far, resulting in a lot of anger, disappointment, passive aggression, and blatant resentment. I am torn. It pays well.

The Blackberry kept buzzing. So I overrode my better judgement and went into the office on Tuesday, and sent the child back to school. I was on my way back home by 1 pm. I booked myself a massage appointment. Work insurance pays for it. That, and paid sick days, are just two of many compelling reasons to stay employed there.

The Blackberry had other ideas, and by 1 pm, I had the laptop back on, and I could not get to my appointment. Work is really challenging these days. While the company itself appears healthy, the work problems I am facing are hard to solve on a good day. We are understaffed, and creative solutions can only stretch my team so far, resulting in a lot of anger, disappointment, passive aggression, and blatant resentment. I am torn. It pays well.

Sunday, April 3, 2011

Pattern recognition

Expenses I am incurring over the next few weeks will appear on my May 2011 Visa statement. I've just registered for the Army Run. Running alone (without the children) and registering early lowers the event cost. Fewer campground bookings will appear this year. The Bluesfest expense is coming due soon. The figure retells my 2010 Visa saga.

Saturday, April 2, 2011

Breaking my own rules

I caved and booked two camping weekends at Ontario provincial parks today. I should have checked my calendar more closely first. The weekend that I booked (this morning) for Murphy's Point overlaps with Bluesfest! This happened to me last year too.

My hope in writing it down here is that I won't do the same thing again next year! The cost of cancelling the booking (this evening) was $16. It's become our annual family tradition to head up to Round Lake when school breaks in June. I kept that weekend booked.

My hope in writing it down here is that I won't do the same thing again next year! The cost of cancelling the booking (this evening) was $16. It's become our annual family tradition to head up to Round Lake when school breaks in June. I kept that weekend booked.

Friday, April 1, 2011

First pass

I just received a draft of my tax return from the accountant. It suggests a refund of $5500. It seemed lower than I was expecting so I checked his math. I have just challenged him (by email) on Line 214 (child care). I've never done that before. If I'm right, it increases the amount of my refund by approximately $2000 and empowers me to clear the credit line.

Looking forward to his response... Seriously!

Update, April 3:

There's a cap based upon the ages of my chidren; it's not an error.

Update, April 4:

The length of time it takes the Canada Revenue Agency to process your income tax return and refund depends on how and when you file your return. Refunds for returns filed electronically before April 15 (as mine just was) are usually processed within two weeks.

Update, April 14:

My tax refund is sitting in my chequing account. Credit line, your days are numbered!

Looking forward to his response... Seriously!

Update, April 3:

There's a cap based upon the ages of my chidren; it's not an error.

Update, April 4:

The length of time it takes the Canada Revenue Agency to process your income tax return and refund depends on how and when you file your return. Refunds for returns filed electronically before April 15 (as mine just was) are usually processed within two weeks.

Update, April 14:

My tax refund is sitting in my chequing account. Credit line, your days are numbered!

Change purse as metaphor

I started my new job in October 2009. My new boss sent me a change purse as a holiday gift a few months later, by overnight courier from San Francisco. I was very touched by the gesture. I kept the purse and started to use it, even though I'd not had need for one before.

From the card, which I kept:

We're so glad that you're here! I know it has been a big change, and that there's a lot of change here all the time. I thought I should send you a little something you can use to keep all that change in. :)

From the card, which I kept:

We're so glad that you're here! I know it has been a big change, and that there's a lot of change here all the time. I thought I should send you a little something you can use to keep all that change in. :)

Today's horoscope for Leo

"You should keep your wallet where it belongs -- locked away in a safe deposit box -- at least until this current wave of weird financial energy passes; you'll see a sign."

I can't make this stuff up. There's 21 cents left in there, and that's my lucky number.

I can't make this stuff up. There's 21 cents left in there, and that's my lucky number.

Thursday, March 31, 2011

Lighter fare

It's payday, and on that note, I've placed the one remaining dollar from my change purse into the 50/50 draw. Let's just say I'm feeling lucky.

Wednesday, March 30, 2011

When that happens...

I broke two weeks worth of insulin pump supplies in five minutes this evening. I have run out of supply on hand, and am currently unable to reattach the medical device without assistance and additional supplies. This is not good. Its directive is to function as a pancreas would. I've switched back to injections until I can reach the nurse for advice.

Update:

Situation under control.

Update, April 1:

Well, not really...

Update, April 3:

Finally, it all seems to be working.

Update, April 4:

Went through another 4 weeks worth of supplies in 10 minutes this morning, but it's attached now. I did it myself. Patience is key.

Update:

Situation under control.

Update, April 1:

Well, not really...

Update, April 3:

Finally, it all seems to be working.

Update, April 4:

Went through another 4 weeks worth of supplies in 10 minutes this morning, but it's attached now. I did it myself. Patience is key.

Tuesday, March 29, 2011

Water from a stone

The skip-a-thon pledge for my youngest is due tomorrow. Her school is raising money for clean water in Africa. I'm giving just a little. These things matter. I should budget for them.

Monday, March 28, 2011

Just did it.

Today I reduced my RRSP contribution from 18% to 8%, effective April 15, without disrupting my current DPSP benefit. The maximum amount of employer matching for the DPSP is 4%. I think this will free up approximately $200 (net) per paycheque.

I paid my coworker the $20 that I owed him for an upcoming concert. He hadn't even noticed that he didn't have it yet. He will be paying for the batch of tickets tomorrow.

I booked a sitter for April 8. I'm going out again. It's a Friday, and it will cost $40.

I paid my coworker the $20 that I owed him for an upcoming concert. He hadn't even noticed that he didn't have it yet. He will be paying for the batch of tickets tomorrow.

I booked a sitter for April 8. I'm going out again. It's a Friday, and it will cost $40.

Sunday, March 27, 2011

Tastes like chicken

Any changes I make to my RRSP contribution won't take effect before mid-April.

I've transferred $500 from the Line of Credit to my chequing account. I think it will cost me less than $3 in interest charges if I pay it back within 30 days. Looking closely at numbers for April, I noticed that I'll exhaust and exceed the overdraft coverage before my mid-April paycheque if I don't transfer funds from somewhere. That could cost me more than $3.

I bought a concert ticket for April 8 at a cost of $39.50, cut my own bangs again, and have painted my toenails a crazy shade of red. It's going to be another long month.

I've transferred $500 from the Line of Credit to my chequing account. I think it will cost me less than $3 in interest charges if I pay it back within 30 days. Looking closely at numbers for April, I noticed that I'll exhaust and exceed the overdraft coverage before my mid-April paycheque if I don't transfer funds from somewhere. That could cost me more than $3.

I bought a concert ticket for April 8 at a cost of $39.50, cut my own bangs again, and have painted my toenails a crazy shade of red. It's going to be another long month.

Sketching out April

Today is Visa statement day: $1880.

My youngest turns six this month which means we have reached ineligibility for the $100 monthly universal child care benefit.

I will be hosting her birthday party on a budget, taking care to keep party costs under $50. A child's party can easily cost $500. It will take some creativity, planning, and a theme like flowers. We can plant seeds, colour pictures of flowers, and make floral crowns from paper, and decorate cupcakes with seeds and stuff to look like flowers. She wants earrings.

New idea: Mad Hatter Tea Party. Seems only fitting. I'll dress her sister up like Alice.

There are five Fridays this month which means we have five $200 daycare cheques going through the chequing account this month.

This might be the last month with an interest payment towards the line of credit debt. That's a good thing, and coincidentally well timed with the UCCB disappearing this month.

I do not have to absorb the diabetic pump start-up costs this month either. That's deferred until the next Visa statement. Whew.

I'd like to cancel the line of credit once it's paid out. My mortgage goes up for renewal in December 2011, and I'll use it as a negotiation point for a better interest rate on a future line of credit. I'll attach it to the same bank that provides my next mortgage.

My chequing account has $500 overdraft protection. I am currently using $485 of it to close up the month of March, and I owe $20 to a coworker for next weekend's concert tickets. I'll try not to think of my six-figure salary as I return wine bottles, and scavenge through desk drawers and coat pockets to make up the difference in change.

The car is due for some maintenance this month. I've got some minor home maintenance planned: redoing the eavestrough caulking and re-attaching trim on a set of double doors.

Bike commuting conserves fuel.

We've started a container garden with seeds and soil on hand. I'm not sure it will yield much if anything, but it's an interesting hobby to share with the girls. We'll add a few more containers to the mix before March is up.

In the absence of the tax refund, something else needs to give to keep the month of April cash flow positive. I'll look at dropping my RRSP contribution to the minimum amount I need to qualify for employer matching. My current contribution sits at 18%.

Until the value of the tax refund is confirmed, the following self-imposed restrictions from January must carry over:

My youngest turns six this month which means we have reached ineligibility for the $100 monthly universal child care benefit.

I will be hosting her birthday party on a budget, taking care to keep party costs under $50. A child's party can easily cost $500. It will take some creativity, planning, and a theme like flowers. We can plant seeds, colour pictures of flowers, and make floral crowns from paper, and decorate cupcakes with seeds and stuff to look like flowers. She wants earrings.

New idea: Mad Hatter Tea Party. Seems only fitting. I'll dress her sister up like Alice.

There are five Fridays this month which means we have five $200 daycare cheques going through the chequing account this month.

This might be the last month with an interest payment towards the line of credit debt. That's a good thing, and coincidentally well timed with the UCCB disappearing this month.

I do not have to absorb the diabetic pump start-up costs this month either. That's deferred until the next Visa statement. Whew.

I'd like to cancel the line of credit once it's paid out. My mortgage goes up for renewal in December 2011, and I'll use it as a negotiation point for a better interest rate on a future line of credit. I'll attach it to the same bank that provides my next mortgage.

My chequing account has $500 overdraft protection. I am currently using $485 of it to close up the month of March, and I owe $20 to a coworker for next weekend's concert tickets. I'll try not to think of my six-figure salary as I return wine bottles, and scavenge through desk drawers and coat pockets to make up the difference in change.

The car is due for some maintenance this month. I've got some minor home maintenance planned: redoing the eavestrough caulking and re-attaching trim on a set of double doors.

Bike commuting conserves fuel.

We've started a container garden with seeds and soil on hand. I'm not sure it will yield much if anything, but it's an interesting hobby to share with the girls. We'll add a few more containers to the mix before March is up.

In the absence of the tax refund, something else needs to give to keep the month of April cash flow positive. I'll look at dropping my RRSP contribution to the minimum amount I need to qualify for employer matching. My current contribution sits at 18%.

Until the value of the tax refund is confirmed, the following self-imposed restrictions from January must carry over:

- electronics

- services related to hair and foot care

- sporting goods

and events - clothing and shoes

- out-of-town travel will be limited to Easter dinner with my parents

- parking

- advance bookings for camp sites (a weekend at Bonnechere in late June and a weekend at Lac Philippe in late August)

- a single Bluesfest pass which is a bargain for this family, when you consider both my kids still get in free. (The concert line-up is announced in late April.)

- the annual Spring Fever impulse drive to Montreal for lunch with the girls

Saturday, March 26, 2011

Clenching my teeth

While I am no accountant, I decided to try out the income tax calculator tool at TaxTips last night. I am expecting to hear the official verdict from my accountant next week.

Assuming I've entered in all the necessary information, the calculator suggests a refund owing of approximately $7000. The amount still borrowed from my line of credit is $6500.

I wondered how much the accountant will charge for his services this year?

Assuming I've entered in all the necessary information, the calculator suggests a refund owing of approximately $7000. The amount still borrowed from my line of credit is $6500.

I wondered how much the accountant will charge for his services this year?

Friday, March 25, 2011

I did not know that

Today I learned that child care costs are not claimed as a non-refundable tax credit, but as a deduction from income on line 214 of the personal tax return.

Although I have had child care expenses in past years, I have never had the proper sort of income from which to deduct them. Self-employment made me ineligible to benefit.

While I did have a little bit of proper employment income in 2009, it was so low that all income tax deducted at source was refunded by the government when I filed my return.

In 2010, a year in which I spent $10600 on child care for my youngest and $2303 for my eldest, my primary source of income has been through my role as full-time employee.

That's the biggest annual child care expense I've incurred to date, and it's probably the peak. It will drop considerably in September 2011 when my youngest starts full-day school.

I also have to compensate my ex-husband for his ineligibility for the credit, as my lower net income disqualified him from claiming it. It was factored into our financial agreement for our child, my eldest and his only. This is not new information, but I hadn't really given it much thought before now, and she's ten. It didn't seem like much, but I guess it adds up.

Although I have had child care expenses in past years, I have never had the proper sort of income from which to deduct them. Self-employment made me ineligible to benefit.

While I did have a little bit of proper employment income in 2009, it was so low that all income tax deducted at source was refunded by the government when I filed my return.

In 2010, a year in which I spent $10600 on child care for my youngest and $2303 for my eldest, my primary source of income has been through my role as full-time employee.

That's the biggest annual child care expense I've incurred to date, and it's probably the peak. It will drop considerably in September 2011 when my youngest starts full-day school.

I also have to compensate my ex-husband for his ineligibility for the credit, as my lower net income disqualified him from claiming it. It was factored into our financial agreement for our child, my eldest and his only. This is not new information, but I hadn't really given it much thought before now, and she's ten. It didn't seem like much, but I guess it adds up.

Tuesday, March 22, 2011

Race against time

The insulin pump supply company suggested I place my first $1000 supply order immediately after starting to use the pump. It meant the order should have been placed last night. The diabetic nurse did not agree when I saw her yesterday and my pump went live.

She suggested I try out some of the various supply options and wait a week before placing the order. It's good advice. Waiting a week should put the expense on next month's Visa statement, not this one. In the meantime, the accountant is busy preparing my tax return.

Fingers crossed for a refund.

Update, March 25:

She still advises I defer placing the order. I'd have drawn from the credit line if I needed it to pay off my incoming Visa bill, but by postponing this expense to the following month's Visa statement, I may not need to.

She suggested I try out some of the various supply options and wait a week before placing the order. It's good advice. Waiting a week should put the expense on next month's Visa statement, not this one. In the meantime, the accountant is busy preparing my tax return.

Fingers crossed for a refund.

Update, March 25:

She still advises I defer placing the order. I'd have drawn from the credit line if I needed it to pay off my incoming Visa bill, but by postponing this expense to the following month's Visa statement, I may not need to.

Biting the bullet

The daycare provider is away for two weeks in July. I need to have a backup plan. The first week I have one child; the second week I will have both. Week one is solved with summer swim camp for the youngest: $183. I'll get back to week two later. Camp for two adds up quickly. I will book time off work or arrange for my parents to return for an extended visit.

Sunday, March 20, 2011

March madness

Today is my last day of vacation. It's been a good week. Trying to get through it without incurring additional costs has been a real challenge. I admit I indulged, just a little:

- on a really nice restaurant dinner with an old flame (we had wine with it)

- on a $22 live theatre ticket (front row of the balcony, not the orchestra)

- on several impulse trips to the grocery store without a list in hand

- on a new T-shirt (very casual, less than $20) from Winners

- on some origami paper and a pair of Hello Kitty yoga pants for my eldest

- having relatives (including both my parents my sister and my niece) visit me

- walking in the nearby woods, while the children hand-fed carrots the deer!

- baking bread with my niece and my youngest

- one-on-one time with my eldest at the bulk food store followed by a bit of shoe shopping (just looking, not buying), while my youngest stayed home to start sunflower plants (in containers) with my father

- dropping by a friend's place on a whim to play a board game on his iPad

- a three-day live test drive of the insulin pump, running saline instead of insulin

- walking around the Byward market on St. Patrick's day toute seule, when patios were open, and stationed with live musicians and people in costumes

- a semi-ritualistic sage cleansing of our home, on the occasion of last's night extreme supermoon, while the children were watching a movie on my iPad

- a trip to Starbucks with my sister, after we reorganized my storage room and she called minimalist me a hoarder (gasp!)

- receiving an unexpected delivery of roses from a male friend who wished to remain anonymous

- watching three decent films via Netflix, while the children were asleep:

Vision, Elling, and War Dance - itemizing tax receipts for the accountant

- running outdoors with the children